E-Invoicing Compliance in France

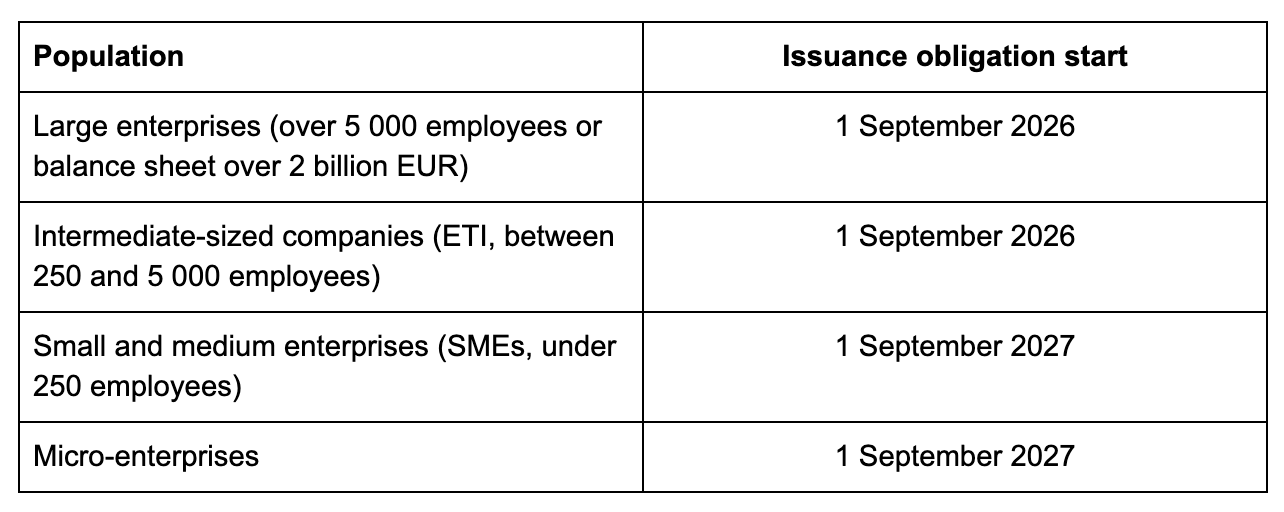

On 1 September 2026, every company subject to French VAT must be able to receive electronic invoices. Large companies and mid-cap groups must also start issuing them. The window for "we will think about it next quarter" is closed. If your French entity has not designated its Plateforme Agréée, has not registered its reception address in the central directory, and has not mapped the four new mandatory invoice mentions onto its ERP outputs, you are no longer ahead of schedule. You are behind.

This page does 2 things. It explains the French e-invoicing reform with the precision your finance team needs to act. And it draws a line that most of the SaaS-driven content on this topic blurs: a compliance provider is not the same thing as a platform vendor. You will need both. They do different jobs. Confusing them is how foreign-owned French entities arrive at September 2026 with a contract for a platform but no actual compliance.

AUDIT

ACCOUNTING

TAXATION

The reform in one paragraph

From 1 September 2026, all VAT-registered companies established in France must be capable of receiving electronic invoices for domestic B2B transactions. From the same date, large enterprises and intermediate-sized companies (ETI) must issue their B2B invoices in electronic format only. The obligation to issue extends to SMEs and micro-enterprises on 1 September 2027. Paper invoices and standard PDFs sent by email become non-compliant, and the only legal channel for transmission is a state-approved platform called a Plateforme Agréée (PA), formerly known as PDP. Source: economie.gouv.fr official page and the DGFiP information portal on impots.gouv.fr.

The reform applies to roughly 10 million economic actors. It rests on a layered legal foundation: Article 91 of the 2024 Finance Law (Loi n° 2023-1322 of 29 December 2023), Article 62 of the 2023 Finance Law, Decree n° 2022-1299 of 7 October 2022, and most recently Article 123 of the Loi de Finances for 2026 (Loi n° 2026-103 of 19 February 2026), which clarified the scope, formalised the abandonment of the public Portail Public de Facturation as a transmission platform, and significantly raised the penalty grid. The April 2025 vote in the National Assembly rejected an amendment proposing a further delay. The 2026 timeline is now firm.

Who is concerned, and what changes

Three obligations come into force on 1 September 2026.

Mandatory e-reporting covers transactions outside the domestic B2B scope: B2C sales, cross-border sales, and certain specific operations. The data is transmitted to the tax authority through the same Plateforme Agréée that handles invoices, on a frequency that depends on the VAT regime of the company.

What is not in scope, with the exclusions formally codified by the Loi de Finances 2026: transactions with foreign customers without French VAT registration (only e-reporting applies), operations carried out by a French taxpayer but located outside the European Union, intra-community deliveries exempt under article 262 ter, I-1° of the General Tax Code (this exclusion is temporary, ending on 1 July 2030 when the EU ViDA framework brings them into scope), transactions exempt from VAT (such as certain financial services), and specific public-sector flows that continue to use Chorus Pro for B2G.

The new infrastructure: PA, annuaire, formats

Three components form the operational backbone of the reform.

Plateforme Agréée (PA)

The PA is a private platform certified by the French tax authority to issue, receive, and route electronic invoices, plus transmit invoice and transaction data to the DGFiP. The platform terminology shifted in July 2025: the original term "PDP" (Plateforme de Dématérialisation Partenaire) is now officially "Plateforme Agréée".

As of early 2026, the DGFiP has approved the first 101 Plateformes Agréées. The list is published and updated on impots.gouv.fr. Notable names include Pennylane, Tiime, Sage, Cegid, Sovos, ClearTax, Esker, Generix, and many more. Each has different strengths: ERP integration depth, sectoral focus, multi-country coverage, pricing structure, treatment of attachments and metadata.

You must designate at least one PA. You can use the same PA for issuance and reception, or split the roles between two providers. You can also change PA later, with no lock-in, as long as the directory entry is updated.

Annuaire central

The Portail Public de Facturation (PPF), originally designed as the state-run free transmission platform, has been redefined. The Government announced in October 2024 that it was abandoning PPF as a transmission tool, and the Loi de Finances 2026 formally codified this abandonment by removing all references to the PPF as a platform from the General Tax Code. Its role is now reduced to that of a central directory (annuaire central) where every company's reception address and chosen PA are listed, and where invoice data flows to the DGFiP for VAT pre-filling and audit purposes. This is a major change foreign CFOs often miss when they read older content from 2022 to 2024.

Approved formats

Three structured formats are approved under the EN 16931 European norm aligned with the EU ViDA directive (VAT in the Digital Age):

Factur-X: hybrid format combining a human-readable PDF with embedded structured XML data. Most common choice for SMEs because it preserves the visual invoice while making the data machine-readable

UBL: pure XML, common in European public procurement and Peppol exchanges

CII: pure XML, used by larger industrial and supply-chain ecosystems

Plain PDFs sent by email are no longer compliant. Direct transmission between supplier and customer outside the PA channel is no longer legal for in-scope transactions.

Four new mandatory invoice mentions

The decree n° 2022-1299, codified in article 242 nonies A of the General Tax Code, requires four new mandatory mentions on top of the existing invoice content. Their effective application date depends on the issuance obligation calendar of each company: 1 September 2026 for large enterprises and ETI, 1 September 2027 for SMEs and micro-enterprises.

The SIREN number of the customer (this serves as the routing key in the central directory)

The category of the operation (delivery of goods, supply of services, or both)

The mention of the option to pay VAT on debits (option pour le paiement de la TVA d'après les débits) when applicable

The full delivery address of the goods, when different from the billing address

Updating ERP and invoicing templates to carry these fields is one of the most underestimated workstreams of the reform. It is also one of the most tested at audit, because absent or incorrect mentions trigger automatic rejection by the receiving PA.

Penalty grid: what the Loi de Finances 2026 actually changed

Article 123 of the Loi de Finances 2026 (Loi n° 2026-103 of 19 February 2026) substantially raised the sanctions framework that had been initially set in 2024. Most foreign-language content on the reform still cites the older figures. The current numbers, codified in article 1737 of the General Tax Code, are the ones that will apply from 1 September 2026.

For the company:

50 EUR per invoice issued in non-electronic format, capped at 15 000 EUR per company per calendar year (raised from 15 EUR)

500 EUR per missing transmission of transaction or payment data (e-reporting), capped at 15 000 EUR per company per calendar year (raised from 250 EUR)

Failure to designate a Plateforme Agréée: the tax authority issues a formal notice (mise en demeure) granting 3 months to comply. If the company is still non-compliant at the end of that period, a 500 EUR fine applies, followed by a new 3-month notice. Persistent non-compliance triggers a 1 000 EUR fine, then 1 000 EUR every additional 3 months until designation is completed

For Plateformes Agréées themselves, the law also raised the bar:

50 EUR per invoice for which a PA fails to transmit data (raised from 15 EUR), capped at 45 000 EUR per year

750 EUR per failed transmission of transaction or payment data, capped at 100 000 EUR per year

New grounds for revocation of the PA registration number, including failure to update the central directory, failure of data portability when a customer changes platform, or failure of minimum service continuity

The penalty framework and its application calendar are detailed on the Service-Public Entreprendre portal maintained by the French government, which directly references the new article 123.

Beyond direct penalties, non-compliance creates collateral business friction: rejected invoices block payment cycles, customers refuse to process non-compliant documents, and the cumulative effect on cash flow can dwarf the formal sanctions.

E-invoicing platform versus e-invoicing compliance partner: the distinction that matters

Two roles, often conflated in marketing material, with very different scopes.

A Plateforme Agréée is a piece of certified technology. It connects to your ERP, validates invoice formats, handles transmission to the recipient PA, manages the 14 transaction statuses (with four mandatory: Submitted, Refused, Payment Sent, Payment Received), and reports to the DGFiP. It is software and infrastructure, sold by a SaaS vendor or by a payments company that has acquired the certification.

A compliance partner is a professional service. It assesses your invoice flows, maps the gaps between your current process and the reform, helps you choose the right PA among the 101+ certified options, configures and tests the integration with your ERP and accounting system, validates the new mandatory mentions, supervises the e-reporting setup for B2C and cross-border flows, registers your company in the annuaire central via a DGFiP-recognised mandate, runs parallel testing before go-live, and stays on call to remediate rejections and audit queries.

You need the platform. You also need the partner. Companies that buy only the platform discover at go-live that their data is misconfigured, their CBA-specific invoicing rules are not handled, and their e-reporting flows are not aligned with their VAT regime. Companies that engage only a partner without choosing a platform have nowhere to route the invoices.

This is where Vachon plays. We are not a Plateforme Agréée and we do not pretend to be. We are an Expert-Comptable inscrit à l'Ordre, formally recognised by the DGFiP since April 2025 as having a central role in the rollout of this reform, with a designated opt-in mandate that lets us register your company's reception address in the central directory on your behalf.

For broader context on our French tax compliance positioning, see our tax compliance services for foreign subsidiaries page.

Compliance readiness checklist for foreign-owned French entities

Six workstreams to close between now and 1 September 2026. If you have not started, you are at the late edge of the comfortable preparation window. Eight to twelve weeks is the minimum for a clean implementation in a mid-sized French entity with one ERP. Multiply for groups with several entities or fragmented systems.

1. Audit current invoice flows. Volume per year, per category (B2B France, B2B EU, B2B export, B2C, exempt), share of inbound vs outbound, current invoice software, current ERP, share of manual versus automated issuance.

2. Map the data quality gaps. SIREN of customers populated correctly, invoice line item structure compatible with Factur-X, treatment of credit notes, deposit invoices, and multi-line consolidations.

3. Select a Plateforme Agréée. Decision criteria covered in the next section.

4. Update ERP and invoicing templates. Add the four new mandatory mentions, ensure VAT category handling is correct, validate the structured data export in Factur-X, UBL, or CII.

5. Configure e-reporting. Identify transactions outside the domestic B2B scope, set the transmission frequency aligned with your VAT filing regime, validate the data points required for B2C and cross-border declarations.

6. Run parallel testing. Before September 2026, send and receive a representative sample of invoices through the PA, simulate rejections and corrections, train the finance team on the new statuses, document the procedures.

We run this six-step program for foreign-owned French entities under a single fixed-fee engagement, with the DGFiP opt-in mandate included.

How to choose a Plateforme Agréée: decision framework

Five criteria that filter the 101+ options to a workable shortlist.

ERP and accounting integration. If your French entity uses Pennylane, choosing Pennylane as your PA simplifies the project. If you run SAP, Oracle, Sage, or Cegid, look for native connectors. If your accounting is on a non-French ERP (NetSuite, Xero, Microsoft Dynamics), validate that the PA has a documented integration path or accepts API ingestion.

Multi-country coverage. If your group operates in Germany, Italy, Spain, Belgium, or Poland, all of which have their own e-invoicing mandates active or coming, a PA with multi-country compliance (Sovos, Avalara, Esker, ClearTax) reduces total cost of ownership. If your French entity is the only EU operation, a France-focused PA is faster and cheaper.

Sectoral specificity. Construction companies, healthcare, agriculture, public utilities, and retail each have invoice particularities (matricule TVA payable on debits, specific attachments, batch invoicing rules). Some PAs are notably stronger in specific verticals.

Pricing structure. Per-invoice pricing, per-user pricing, fixed fee, freemium with paid premium. The cost ranges from zero (some PAs are free for simple cases) to 5 EUR per invoice or more for high-touch enterprise setups.

Roadmap on the EU ViDA directive. The French reform is one chapter of a wider EU initiative. PAs that have a clear roadmap on Peppol interoperability and on the upcoming EU-wide e-reporting framework are safer long-term bets.

We do not have a preferred PA. We work with whichever PA fits the client's stack best, and we have integration experience with the major French and multi-country options.

Why Vachon is the right e-invoicing compliance partner for foreign groups in France ?

Three reasons that come up consistently with our clients.

Expert-Comptable inscrit à l'Ordre with the DGFiP-recognised mandate. As confirmed by the President of the Ordre des Experts-Comptables in April 2025, the DGFiP officially recognises the central role of chartered accountants in the rollout of this reform. The opt-in mandate that lets us register your company's reception address in the central directory is built into the reform infrastructure. SaaS vendors do not have this status.

Bilingual operations integrated with the rest of your French compliance stack. E-invoicing does not sit alone. It connects to VAT filing (where pre-filling will eventually flow from invoice data), to corporate income tax through the audit trail it creates, to bookkeeping (10-year retention obligations for invoices), and to payroll only at the margin. Running e-invoicing inside a firm that also handles your bookkeeping, your tax compliance, your payroll and tax management, and your chartered accountant relationship closes the seams that fragmented setups leak through.

Senior partner involvement on every reform-mapping engagement. The 2026 reform is not a routine compliance task. It is a one-time architectural change with material long-tail consequences. Our reform-mapping engagements are led by partners, not by junior preparers, and the deliverable is a documented compliance posture you can show to your group auditor or your incoming tax inspector without reserve.

We have been the French CPA partner of foreign groups since 1997. The 2026 reform is the largest French invoicing change since the introduction of mandatory VAT registration. Treat it accordingly.

Get your French entity ready before September 2026 lands

If your French entity has not started the e-invoicing project, or if the project is open but stalled in platform selection, the next move is a 90-minute scoping session with our compliance team. We will map your current invoice flows, identify the four to six workstreams that matter for your specific case, and give you a fixed-fee implementation plan you can take to your board.

Frequently asked questions

When does e-invoicing become mandatory in France?

On 1 September 2026 for reception by all VAT-registered companies and for issuance by large enterprises and ETI. On 1 September 2027 for issuance by SMEs and micro-enterprises.

Is the 2026 deadline final?

Yes. The April 2025 vote in the National Assembly rejected an amendment to delay the reform further. The current calendar is firm.

What is a Plateforme Agréée?

A private digital platform certified by the French tax authority to issue, receive, and route electronic invoices in approved formats (Factur-X, UBL, CII), and to transmit invoice and transaction data to the DGFiP. The term replaces the original PDP designation since July 2025. The DGFiP has approved more than 101 Plateformes Agréées as of early 2026.

Can a foreign company send electronic invoices to a French customer?

Foreign suppliers without French VAT registration are not yet required to issue electronic invoices and can continue sending PDFs by email. Foreign companies VAT-registered in France through a French entity are in scope of the reform on the same timeline as domestic companies.

What happens to the Portail Public de Facturation (PPF)?

The PPF is no longer a transmission platform. The Government announced its abandonment in October 2024, and the Loi de Finances 2026 formally codified this by removing all references to the PPF as a platform from the General Tax Code. Its role is now limited to operating the central directory (annuaire central) of reception addresses and to centralising data for the DGFiP. All invoice transmission goes through Plateformes Agréées.

What are the penalties for non-compliance?

Under article 123 of the Loi de Finances 2026, fines were raised across the board: 50 EUR per invoice issued in non-electronic format, 500 EUR per missing e-reporting transmission, both capped at 15 000 EUR per company per year. For failure to designate a Plateforme Agréée, a 3-month formal notice is followed by a 500 EUR fine, then 1 000 EUR per quarter of continued non-compliance.

What did the Loi de Finances 2026 change?

Loi n° 2026-103 of 19 February 2026 (article 123) clarified the scope of the reform, formally codified the abandonment of the PPF as a transmission platform, and significantly raised the penalty grid. Fines on companies tripled (from 15 to 50 EUR per non-compliant invoice) and doubled on e-reporting failures (from 250 to 500 EUR). The law also tightened obligations on Plateformes Agréées, with new grounds for revocation of their registration.

Is e-reporting the same as e-invoicing?

No. E-invoicing covers domestic B2B transactions and uses structured invoice formats routed through a PA. E-reporting covers transactions outside the domestic B2B scope (B2C, cross-border, certain specific operations) and transmits transaction and payment data to the DGFiP without an actual invoice flowing through the system.

Can my expert-comptable handle the registration in the central directory for me?

Yes. Since April 2025, the DGFiP has formalised an opt-in mandate that allows your chartered accountant to register your company's reception address in the central directory on your behalf. This mandate can be included in the engagement letter.

Does Vachon operate a Plateforme Agréée?

No. We are an Expert-Comptable, not a platform vendor. Our role is to advise on the choice of PA, configure and test the integration, manage the directory registration via the DGFiP-recognised mandate, supervise e-reporting setup, and ensure ongoing compliance. The platform itself is provided by your chosen PA.

How long does a clean compliance setup take?

Eight to twelve weeks for a mid-sized French entity with one ERP and standard invoice flows. Longer for groups with multiple entities, fragmented systems, or specific sectoral rules. Engagements started after July 2026 carry significant execution risk for the September deadline.