Fiscal Representative in France

A non-EU company sells goods to French customers. A US e-commerce brand stores stock in a Paris-region warehouse. A Swiss manufacturer imports machinery into Le Havre. None of them has a French entity. All three may be required, by French law, to appoint a fiscal representative in France before they can register for VAT, file a single return, or recover a single euro of input tax.

This page is a working guide to that obligation. What it is. Who actually needs one. The 41 countries that are exempt. What changed on 1 January 2026 (because something significant did). And the cost of getting it wrong, which in France is calculated on the representative's own balance sheet because of joint liability.

We do not approach this topic as a SaaS vendor. Vachon is a French CPA and audit firm, founded in 1997, working almost exclusively with foreign-owned French operations. The fiscal representative question lands on our desk every month, often after a botched first registration. The information below is what we would tell you in a 30-minute scoping call.

AUDIT

ACCOUNTING

TAXATION

What a fiscal representative actually is

A fiscal representative (in French, représentant fiscal) is a French-established taxable person, accredited by the French tax authority, who agrees to assume all VAT obligations on behalf of a foreign company that is liable for French VAT but has no establishment in the European Union. The legal foundation sits in article 289 A of the French General Tax Code, as updated by successive finance laws

The role carries three defining characteristics that separate it from a simpler tax agent:

Joint and several liability: the representative is personally liable for the represented company's VAT debts, late-payment interest, and penalties. If the foreign client defaults, the French tax authority can collect from the representative directly

Single-point accountability: the representative is the sole interlocutor for the DGFiP, signs the registration, files every return, manages refunds, and handles audits

Local establishment requirement: the representative must be a French taxable person with sufficient organisation, financial solvency, and professional standing to carry the role

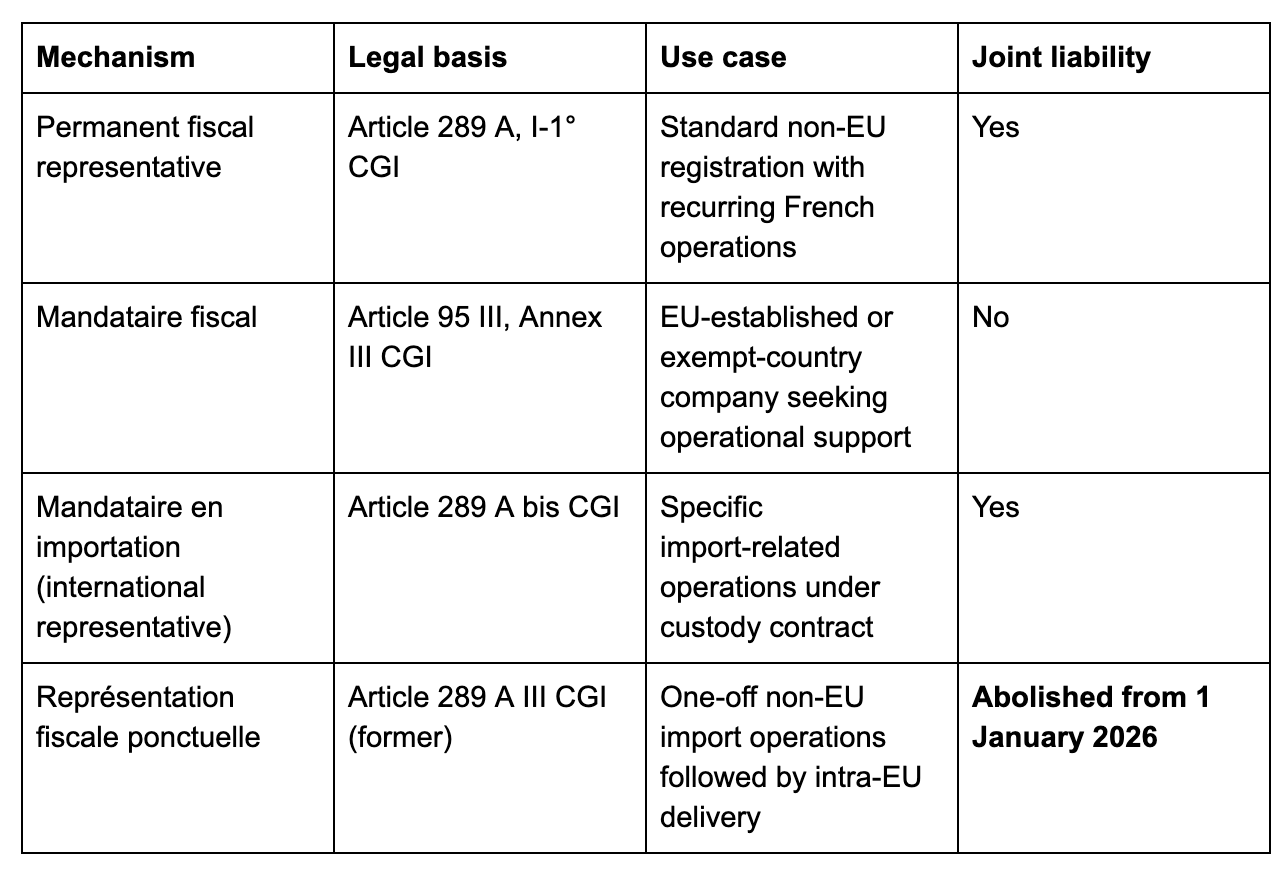

Do not confuse a fiscal representative with two adjacent roles that French law treats differently. A mandataire fiscal is an agent without joint liability, used by EU-established companies that prefer a French operational contact. A mandataire en importation is an import agent under article 289 A bis, applicable in narrowly defined import scenarios. The three roles serve different cases, carry different responsibilities, and cost different amounts.

Who is required to appoint one ?

The decision logic comes in 3 layers. Walk through them in order.

Layer 1: where is your company established?

Established in the EU: you do not need a fiscal representative in France. You can register for VAT directly with the Direction des Résidents à l'Étranger et des Services Généraux (DRESG) in Noisy-le-Grand. You may, optionally, appoint a mandataire fiscal without joint liability for operational convenience

Established outside the EU but in a country with a mutual assistance agreement with France: you are exempt. You register directly, like an EU-established company. The list is in the next section

Established outside the EU and outside the exempt list: you must appoint a fiscal representative under article 289 A, I-1° of the CGI, before you can register for French VAT

Layer 2: do you actually have French VAT obligations?

A foreign company is required to register for French VAT, with or without a representative depending on Layer 1, when one or more of the following is true:

You hold stock in France (including third-party fulfilment warehouses, Amazon FBA centres, 3PL hubs)

You make distance sales of goods to French consumers above the EU OSS thresholds without using OSS

You provide certain services that are taxable in France under the place-of-supply rules

You carry out intra-Community deliveries from France to other EU countries

You receive a VAT refund claim under the 13th Directive (non-EU companies)

Without one of these triggers, the question of fiscal representation is moot. With one of them, Layer 1 dictates the path.

Layer 3: which mechanism applies to your specific case?

Multiple mechanisms exist within the broader fiscal representation framework. They are not interchangeable. Picking the wrong one delays registration by 4 to 8 weeks.

The 41 exempt countries: who can register without a fiscal representative

The exemption rests on article 289 A, I-1° of the General Tax Code and is materialised by the arrêté du 15 mai 2013, last updated by the arrêté du 16 février 2021. The full list, in alphabetical order:

Antigua and Barbuda, Argentina, Armenia, Aruba, Australia, Azerbaijan, Bosnia and Herzegovina, Cape Verde, Cook Islands, Curaçao, Dominica, Ecuador, French Polynesia, Faroe Islands, Georgia, Ghana, Greenland, Iceland, India, Jamaica, Japan, Kenya, Mauritius, Mexico, Moldova, Monaco, Montserrat, Nauru, New Caledonia, New Zealand, Nigeria, Niue, North Macedonia, Norway, Pakistan, Saint-Barthélemy, Saint Martin (French side), San Marino, Sint Maarten, South Africa, South Korea, Tunisia, Turkey, Uganda, Ukraine, United Kingdom, Uzbekistan, Vanuatu, Wallis and Futuna.

(Note: the exact count fluctuates as governments sign or modify mutual-assistance instruments. Check the latest version of the arrêté before relying on this list for a registration. Source: Légifrance, arrêté of 16 February 2021.)

2 takeaways for cross-border tax teams:

Brexit shifted the UK into the exempt list in 2021. UK-established companies have not needed a French fiscal representative since the arrêté du 16 février 2021 added the United Kingdom to the list. They register directly, like an EU company

United States, China, Switzerland, Hong Kong, Singapore, Brazil are NOT on the list. Companies established in these jurisdictions must appoint a fiscal representative if they trigger a French VAT obligation

If your country sits outside both the EU and the exempt list, factor the cost and joint-liability exposure into your French market-entry plan from the start. It is not a marginal cost.

What changed on 1 January 2026: the end of one-off fiscal representation

This is the most consequential French VAT change for non-EU importers in a decade, and it is poorly covered in English-language sources.

The représentation fiscale ponctuelle (one-off fiscal representation) regime, codified in former article 289 A III of the CGI, was repealed by article 112 of the Loi de Finances for 2024 (Loi n° 2023-1322 of 29 December 2023), with effect on 1 January 2026. The French tax authority granted an exceptional extension to 31 December 2025 for taxpayers who had initiated a French registration before that date, but the regime is now closed.

What it used to allow: a non-EU company importing goods into France and immediately re-shipping them to another EU member state under Customs Procedure 42 could borrow the VAT number of a French fiscal representative for the single transaction, without registering for VAT itself.

What is required now: any non-EU company using Customs Procedure 42 in France must obtain its own French VAT number and appoint either a permanent fiscal representative under article 289 A or an international representative under the new article 289 A bis. The administrative threshold has risen materially.

Article 289 A bis CGI, in force since 1 January 2025, introduced the international representative mandate alongside the regime above. It allows a non-EU taxpayer who is not VAT-registered in France to delegate all VAT reporting and payment obligations to a French-established representative, provided the representative has physical control of the goods under a specific custody contract. The mechanism is narrow: it applies only to taxpayers under a contrat de dépôt arrangement and not, currently, to Customs Procedure 42 operations. Source: Paradigmes Avocats analysis of Customs Procedure 42.

If your supply chain into France runs through Customs Procedure 42, the planning conversation with a French CPA needs to happen now, not at year-end.

What a fiscal representative actually does for you ?

The job description, written from the standpoint of what you should expect to receive month after month, not what a brochure promises:

Initial accreditation file submitted to the DGFiP, including the representative's authorisation, the foreign company's articles, and proof of activity in France

French VAT registration (form EE0, then VAT-specific paperwork), obtaining your French intra-Community VAT number (FR XX 999 999 999)

EORI number coordination when import operations are involved

Monthly or quarterly VAT returns (form CA3) filed via the impots.gouv.fr professional portal, by the 19th to 24th of M+1 depending on legal form and country

Intrastat (DEB) filings when intra-Community thresholds are crossed

Recapitulative statements (DES) for intra-Community supplies of services

VAT refund coordination under the 13th Directive for non-EU clients, with the additional requirement of fiscal representation for the refund itself

Liaison and defence in DGFiP audits and queries, in French, with full documentation of every transaction

Joint-liability monitoring: the representative reviews supporting documents (invoices, customs declarations, transport documents) before validating the periodic return, because their own balance sheet is exposed if data is wrong

Bookkeeping for the represented company's French VAT operations must be kept in France, in French, for 10 years, available on demand for tax inspection.

The cost of fiscal representation, and why it is not commodity pricing

Fiscal representation is not a transactional service. The representative is signing for your VAT debts. Pricing reflects this.

3 components in a typical engagement:

Set-up fee: 1 500 to 5 000 EUR, covering the accreditation file, registration, and onboarding

Annual representation fee: 4 000 to 12 000 EUR per year, depending on transaction volume and complexity. Some providers price per filing, others on a fixed annual basis

Bank guarantee or financial security: many representatives require a bank guarantee or cash deposit equivalent to 1 to 3 months of expected VAT payable, as protection against the joint-liability exposure. This is a working capital lock-up that needs to be sized into your French operations plan

Beware of providers offering fiscal representation at SaaS-style prices (under 2 000 EUR per year all-in). Either the fine print transfers liability back to you contractually, or the provider has not understood what they are signing for. Both end badly.

For a related conversation on broader French VAT compliance beyond representation, our tax compliance for foreign subsidiaries page and the tax consulting in France page cover the wider perimeter.

5 mistakes we keep cleaning up

Recurring patterns from foreign-owned operations that arrived at Vachon mid-issue, in rough order of frequency:

Registering through the wrong mechanism. A US e-commerce brand registers as a mandataire fiscal via a friendly French accountant, then discovers two years later that they should have had a permanent fiscal representative under article 289 A. Retroactive regularisation, joint-liability cleanup, often penalties.

Underestimating joint-liability transfer in the contract. Some non-French providers transfer the joint liability back to the foreign client through indemnity clauses. The French tax authority does not care about your private contract. They collect from the registered representative. The representative collects from you. The chain of recourse takes years if it works at all.

Ignoring the bank guarantee until the registration is blocked. The representative cannot accredit you without the financial security in place. A 90-day delay because the corporate treasury team did not size the guarantee into the plan is the most common cause of missed go-live dates.

Mishandling the Brexit transition. UK-established companies that appointed a French fiscal representative in 2021 still have one on the books in some cases, because nobody updated the registration after the arrêté du 16 février 2021 removed the requirement. The result is unnecessary annual fees and unused joint liability.

Treating the 13th Directive refund as a self-service operation. A non-EU client claims a 13th Directive VAT refund without a fiscal representative in place, then wonders why the refund is denied. The DGFiP requires fiscal representation for the refund itself. No representative, no refund.

Vachon's role on fiscal representation engagements

We work with foreign-owned French operations across the full perimeter of French tax and accounting. On fiscal representation specifically, our involvement falls into one of three patterns:

Direct fiscal representation services, when the engagement fits our risk and operational profile. We handle the accreditation, the registration, the recurring filings, the audits, with the same partners and the same bilingual reporting your CFO already uses for the rest of the French stack.

Coordination with a specialist fiscal representative, when transaction volumes or sectoral specifics (excise goods, energy, pharma) call for a dedicated representation firm. We sit between you and the representative, validate the data flowing into the returns, and integrate it with the VAT compliance and bookkeeping work we are already doing.

Audit and remediation, when a foreign-owned French operation arrives with a fiscal representation issue already in motion: a DGFiP audit, a refund denial, a misregistration, a Brexit holdover. We assess, we document, we negotiate.

The goal across all three patterns is the same: get you to a clean French VAT posture, integrated with the rest of your French statutory obligations, with one bilingual partner accountable end-to-end. Our english-speaking chartered accountant team is structured around exactly this kind of cross-border interface.

Get a clean answer for your specific case

If your company is preparing to enter the French market, has just discovered an unmet French VAT obligation, or has inherited a fiscal representation setup that needs review, the next step is a 30-minute scoping call with our team. We will ask seven questions, identify your applicable mechanism, give you a realistic cost and timeline, and tell you whether you need representation at all (some companies discover they do not).

Frequently asked questions

What is a fiscal representative in France?

A French-established taxable person, accredited by the DGFiP under article 289 A of the General Tax Code, who acts on behalf of a non-EU company liable for French VAT and assumes joint and several liability for that company's French tax debts.

Is a fiscal representative mandatory for non-EU companies?

Yes, unless the company is established in one of the 41 countries listed in the arrêté du 15 mai 2013 (as updated in 2021) with which France has a mutual-assistance agreement. Companies in those countries register directly without a fiscal representative.

Do UK companies need a French fiscal representative after Brexit?

No. The United Kingdom was added to the exempt list by the arrêté du 16 février 2021, which entered into force on 27 February 2021. UK-established companies register for French VAT directly, like EU companies, without joint liability on a French intermediary.

Do US, Chinese, or Swiss companies need a French fiscal representative?

Yes, when they trigger a French VAT obligation (imports, French stock, distance sales above thresholds, taxable services). The United States, China, and Switzerland are not on the exempt list.

How long does it take to appoint a fiscal representative and obtain a French VAT number?

Typically 4 to 8 weeks from full documentation to active VAT number, depending on the DGFiP backlog and the complexity of the bank-guarantee setup. Incomplete files can extend this to 12 weeks.

What changed on 1 January 2026 for fiscal representation in France?

The représentation fiscale ponctuelle (one-off fiscal representation) regime under former article 289 A III of the CGI was abolished by article 112 of the Loi de Finances for 2024, effective 1 January 2026. Non-EU companies using Customs Procedure 42 in France now need a full French VAT registration and a permanent fiscal representative under article 289 A.

What is the new article 289 A bis "international representative"?

In force since 1 January 2025, article 289 A bis allows a non-EU taxpayer who is not VAT-registered in France to delegate all VAT reporting and payment obligations to a French-established representative, on the condition that the representative has physical control of the goods under a specific custody contract. The mechanism is narrow and does not currently apply to Customs Procedure 42 operations.

Can my regular French accountant act as my fiscal representative?

Only if the firm meets the DGFiP's requirements: registration as a French taxable person, sufficient operational organisation, financial solvency, professional standing, and willingness to assume joint liability. Many CPA firms decline the role precisely because of the joint-liability exposure.

How much does a fiscal representative cost in France?

Set-up fees typically run from 1 500 to 5 000 EUR. Annual representation fees range from 4 000 to 12 000 EUR depending on transaction volume. Plus a bank guarantee or cash deposit equivalent to 1 to 3 months of expected VAT payable.

Can I cancel my fiscal representation arrangement?

Yes, with proper notice and after settling all open VAT positions. Termination requires coordination with the DGFiP and the appointment of a successor, or deregistration from French VAT if your activity has ended. The outgoing representative remains liable for periods under their representation.