Foreign Employer Payroll in France

You hired your first employee in France. The contract is signed, the start date is locked, and your CFO just asked the question that makes most non-French companies freeze: who actually runs the payroll?

If your company is registered abroad and has no establishment on French soil, you are not stuck. France has a dedicated administrative regime for your exact situation. It is functional, it is legal, and it has been used by thousands of foreign companies since 2004. It is also one of the most misunderstood mechanisms in European cross-border employment.

This page explains how to run foreign employer payroll in France when you do not have, and do not want, a French legal entity. It compares the three viable routes, walks through the URSSAF registration process, and flags the compliance traps that turn a clean hire into an expensive audit.

What "foreign employer payroll in France" actually means ?

A foreign employer payroll arrangement applies when a company headquartered outside France employs a person who lives in France and performs their work on French soil, without the foreign company holding any establishment, branch, or subsidiary in the country.

Under the French Social Security Code and EU Regulations 883/2004 and 987/2009, the location of the work, not the headquarters of the employer, determines which social security regime applies. As soon as the employee's habitual workplace is France, French social security applies, French labour law applies, and contributions are owed to the French collection bodies.

The employer remains foreign. The employment contract remains a contract of the foreign company. But payroll is processed under French rules, with French rates, on French calendars.

The single point of entry for these obligations is the URSSAF Service Firmes Étrangères, which is part of URSSAF Alsace and based in Strasbourg.

AUDIT

ACCOUNTING

TAXATION

When this regime applies to you ?

3 triggers, any of which puts you in scope

You hire a person who is resident in France and will perform their work primarily on French territory

Your employee works simultaneously across several EU member states and qualifies for French affiliation under the substantial activity or residency criteria of EU Regulation 883/2004

You temporarily send a worker to France who does not qualify for the secondment certificate (A1) and therefore falls under the French regime

For details on the international rules, the Centre des Liaisons Européennes et Internationales de Sécurité Sociale (Cleiss) is the authoritative French reference, and we recommend reading their employer pages before any cross-border hire.

Three situations are out of scope and need a different route:

Monaco-based companies (handled by URSSAF Provence-Alpes-Côte d'Azur)

Live entertainment producers hiring artists or technicians (handled by Guso)

Bullfighting professionals (URSSAF Languedoc-Roussillon)

If your foreign company already has an establishment in France, you are not in this regime at all. You declare and pay through the standard URSSAF channel of the region where each establishment is located, and our payroll services for French subsidiaries page is the right starting point.

3 routes for foreign employers, ranked by what they actually cost you

You have three legitimate options. The right one depends on headcount, growth horizon, and your appetite for administrative work.

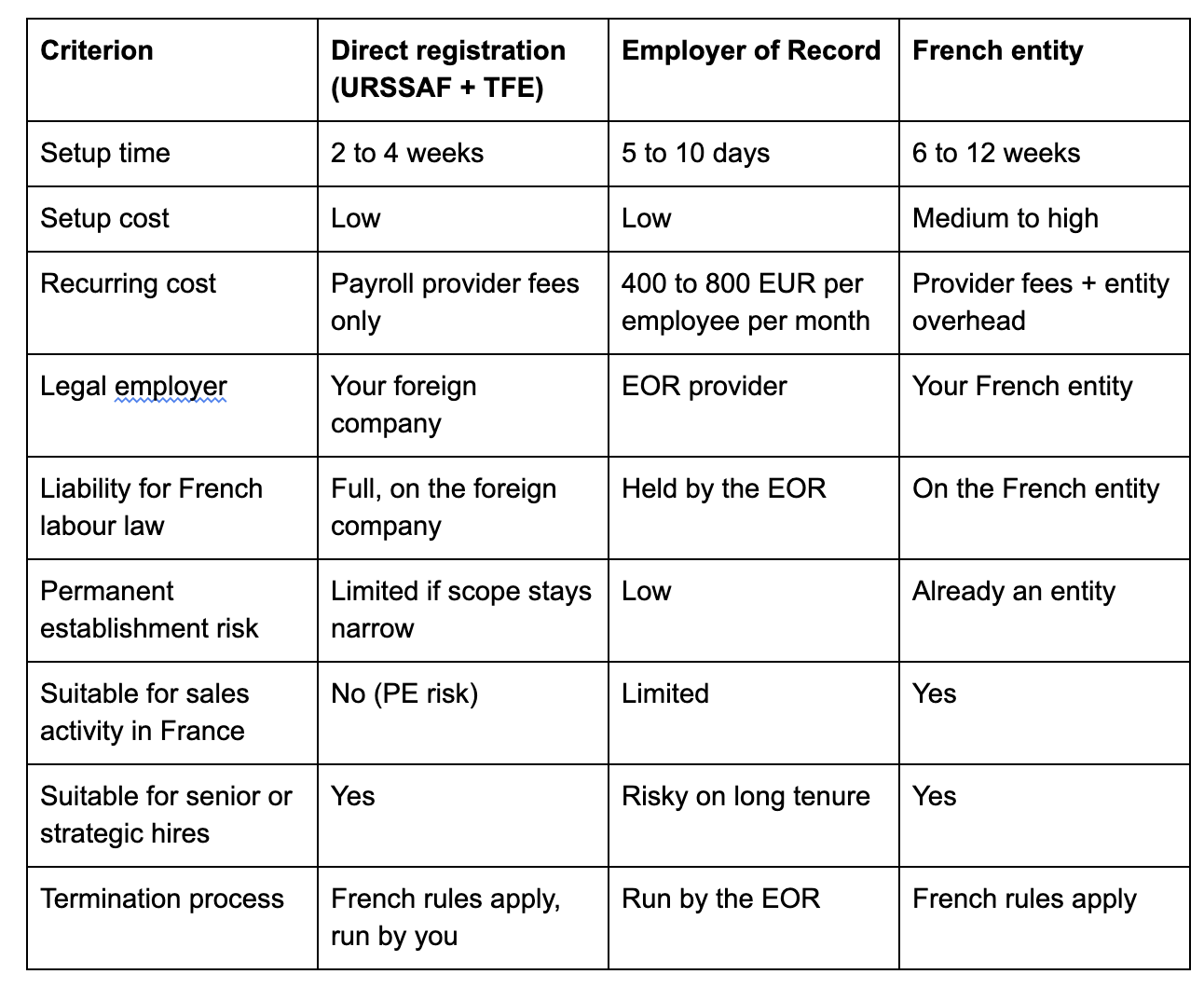

Route 1: Direct registration as a foreign employer (URSSAF Service Firmes Étrangères + TFE)

You register your foreign company directly with URSSAF Alsace, obtain a French SIRET number, and run payroll in your own name. The optional Titre Firmes Étrangères (TFE) scheme bundles registrations and declarations into a single online portal.

Best for: companies hiring 1 to 5 French employees, no plans for a local presence, predictable headcount.

Watch out for: you remain the legal employer, with full liability for French labour law, collective bargaining agreements, and termination rules. You need French-speaking expertise on call, or a local payroll advisor.

Route 2: Employer of Record (EOR)

A third party becomes the legal employer of record on French soil. You direct the work; they hold the contract.

Best for: very fast hiring, short-term tests of the French market, or single hires where you want zero compliance exposure.

Watch out for: monthly fees of 400 to 800 euros per employee, no direct contractual relationship between you and your worker, structural co-employment risk if you exceed 12 to 18 months on the same person, and friction at the moment you eventually want to bring the employee back into your own structure.

Route 3: French legal entity (subsidiary or branch)

You incorporate a French entity, register it with the Commercial Court, and run payroll the standard way.

Best for: sustained hiring (5+ employees), commercial activity in France, long-term presence.

Watch out for: 6 to 12 weeks of setup, share capital, statutory accounts in French GAAP, corporate tax filing, statutory auditor obligations above thresholds. This is a strategic investment, not a workaround.

Side-by-side decision framework

The honest call: if you plan to hire 1 to 3 employees in France for the next 18 months, with no commercial activity on French soil, direct registration via TFE is usually the cheapest, cleanest, and most autonomous option. If you need to hire tomorrow morning and you are not willing to spend a single hour on French paperwork, EOR earns its premium. If you are building a commercial presence, an entity is not optional, it is the only structurally sound choice.

How URSSAF registration actually works for foreign employers

The process is more bureaucratic than complex. Six steps, in order.

1. Submit form EE0 to URSSAF Alsace

The EE0 form opens your file with the Centre National des Firmes Étrangères (CNFE). The CNFE forwards your registration to INSEE, which issues your French SIRET number, and to the relevant social security and pension bodies (Carsat, Malakoff Humanis Agirc-Arrco for supplementary pension, Direction des impôts des non-résidents for income tax).

Allow 3 to 6 weeks from EE0 submission to active SIRET, depending on document completeness.

2. Sign a French-compliant employment contract

Even though the employer is foreign, the contract must comply with the French Labour Code and the Collective Bargaining Agreement (Convention Collective) that applies to your employee's role. The official version of the contract must be in French. A bilingual version with a French original is standard practice.

Identifying the right CBA is the single most underestimated step. France has more than 200 active collective agreements, most of which set minimum salaries, paid leave, notice periods, and termination indemnities above the Labour Code baseline. Applying the wrong CBA, or none, is a frequent and expensive mistake.

3. File the DPAE before the employee starts

The Déclaration Préalable à l'Embauche (DPAE) must be filed online via net-entreprises.fr at least 8 days before the contractual start date. It registers the employee with the French social security system and triggers occupational health checks.

4. Choose your declaration channel: TFE or DSN

Two options for monthly declarations:

TFE (Titre Firmes Étrangères): a free, simplified URSSAF portal. You enter the salary elements; URSSAF calculates social contributions, generates a payslip, and produces an annual tax statement. One transfer to URSSAF Alsace, who then redistributes to all other bodies. Reference: tfe.urssaf.fr

DSN (Déclaration Sociale Nominative): the standard monthly employer declaration used by all French companies, filed via payroll software. More flexible, more granular, mandatory if you use a payroll provider. You handle separate transfers to each body.

TFE is genuinely simple if your situation is simple: standard CDI, one or two employees, no complex variable pay. The moment you have multi-component compensation, equity, expatriate allowances, or industry-specific benefits, TFE becomes a constraint and DSN through a payroll partner is more efficient.

5. Withhold income tax at source (Prélèvement à la Source)

Since 2019, French employers withhold personal income tax directly from net salary using the rate transmitted by the French tax authority. As a foreign employer, you remit this withholding monthly to the Direction Générale des Finances Publiques. TFE handles this calculation automatically. With DSN, your payroll provider handles it.

6. Pay supplementary pension and any sector-specific contributions separately

Mandatory supplementary pension (Agirc-Arrco) is collected by Malakoff Humanis International for foreign employers. Construction sector employers also owe paid leave and weather-stoppage contributions to the relevant caisse de congés payés. These obligations sit outside TFE and need a separate process.

The real cost of employing in France as a foreign employer

The total employer cost is not your headline gross salary. France has one of the highest social charge ratios in the OECD, and the calculation is layered.

Mandatory employer social contributions

For 2026, employer social contributions for non-resident employers without establishment in France typically range from 25% to 45% of gross salary, depending on salary level (multiple thresholds tied to the PASS, the social security ceiling) and risk classification. The detailed rate grid is published on the dedicated URSSAF portal for foreign companies at foreign-companies.urssaf.eu.

The 2026 occupational accident rate (AT) for foreign employers without establishment is set at 0.73% (risk code 511TH) for standard employees and 0.79% for VRP sales staff.

What you do not pay as a foreign employer without establishment

Article L.6131-1 of the Labour Code exempts foreign employers without establishment in France from:

Apprenticeship tax (taxe d'apprentissage)

Continuing professional training contributions (contributions à la formation professionnelle)

This is a meaningful saving compared to a French entity, and one of the genuine cost arguments in favour of staying without establishment.

What you do pay that you might not expect

The 13th-month bonus, often imposed by collective bargaining agreement, even though not a statutory rule

Employer-funded complementary health insurance (mutuelle), mandatory at minimum 50% employer share

Mandatory pension top-up via Agirc-Arrco for cadre and non-cadre employees

Paid leave at 5 statutory weeks plus RTT days for employees on reduced-hour contracts

The CSG/CRDS social levies on remuneration

For a precise total cost simulation tied to your specific case, our payroll advisory team builds a fully loaded gross-to-net-to-employer-cost model before you sign the contract, not after.

5 compliance traps that cost foreign employers the most

These are the recurring failures we see across audit and remediation work.

Permanent establishment exposure. A French employee performing commercial functions, signing on behalf of the foreign company, or maintaining a fixed place of business at home can trigger a permanent establishment under French tax law. You then owe French corporate tax, not just payroll. This is the single most expensive trap. Roles must be carefully scoped and documented from the contract stage.

Wrong collective bargaining agreement. Every foreign employer must declare the applicable CBA. Picking it wrong, or skipping the question, exposes you to retroactive salary top-ups, paid leave catch-up, and disputes at the labour court (Conseil de Prud'hommes).

Late or missed DSN/TFE filings. Penalties start at 1,500 euros per infraction and accumulate quickly. DSN deadlines are monthly, on the 5th or 15th of the following month depending on company size.

Misclassifying the employee as a contractor. France looks at the substance of the working relationship, not the contract label. An "independent contractor" who works exclusively for you, on your tools, on your hours, will be reclassified as an employee, with retroactive social charges, paid leave, and severance.

Botched termination. French dismissal procedures are formal: written notice, motivation letter, prior interview, statutory indemnities. Foreign employers improvising termination by foreign-style email face damages of 6 to 24 months of salary at Prud'hommes.

For sustained mitigation across these risks, our payroll management services are designed around the audit-ready posture that foreign employers need from day one.

Why foreign companies bring this work to Vachon ?

Vachon Group is a French CPA and audit firm based in Paris, founded in 1997, with a team of around 40 professionals dedicated almost exclusively to international companies operating in France. We are a founding member of the AICPA international council, which is uncommon for a French firm and reflects how seriously we take the dual-standard reporting that foreign parents require.

For foreign employer payroll specifically, three things matter, and we deliver them:

One bilingual contact who speaks the language of your CFO and the language of URSSAF Strasbourg, and who does not hide behind a ticket system

A choice of TFE or DSN routing depending on what genuinely fits your case, not what is easiest for the provider

Integration with parent reporting under both French GAAP and US GAAP or IFRS, which our GAAP reconciliation page describes in detail

We do not run an EOR. We are not a HR-tech platform. We are the French payroll and tax partner foreign companies retain when they want this done correctly, audited cleanly, and explained without acronym fog.

Frequently asked questions

Can a foreign company pay an employee in France without a French entity?

Yes. The foreign company registers directly with URSSAF Service Firmes Étrangères, obtains a French SIRET number, and processes payroll under French rules. The optional TFE scheme simplifies declarations.

What is the TFE scheme?

The Titre Firmes Étrangères is a free URSSAF portal designed specifically for foreign companies without an establishment in France. It bundles the DPAE, payslip generation, social contribution calculation, and income tax withholding into a single online interface, with one monthly transfer to URSSAF Alsace.

How long does URSSAF registration take for a foreign employer?

Allow 3 to 6 weeks from submission of the EE0 form to receipt of an active SIRET, depending on documentation quality and current CNFE backlog.

Do I need to pay French corporate tax if I employ someone in France?

Not automatically. Employing one or more people in France does not by itself create a permanent establishment, but it can if the employee performs commercial activity, signs contracts on your behalf, or operates from a fixed place of business. The scope of the role determines the answer.

Is an Employer of Record cheaper than registering directly?

Rarely, beyond very short engagements. EOR fees of 400 to 800 euros per employee per month exceed the cost of direct registration with a payroll partner once you cross 12 to 18 months of tenure or hire more than 2 employees.

Which collective bargaining agreement applies to my French employee?

The CBA is determined by the principal activity of your company on French soil, not by your headquarters' industry classification. Identifying it requires a case-by-case analysis based on the employee's tasks and the company's economic activity. We handle this assessment on every onboarding.

Are foreign employers exempt from any French payroll taxes?

Yes. Foreign employers without an establishment in France are exempt from the apprenticeship tax and the continuing professional training contributions, under article L.6131-1 of the Labour Code. They remain liable for all standard social security contributions.

What happens if I want to bring a foreign employer arrangement to an end?

Termination follows French labour law in full, including notice, statutory indemnities, and procedural requirements. The fact that the employer is foreign does not soften the rules. Plan terminations with French legal support from the start.

Run your French payroll from a single point of contact

If you are about to hire your first employee in France, or you already are and the paperwork has stopped feeling manageable, we can take it from here. Contact our payroll team for a 30-minute scoping call. We will tell you which route fits your case, in numbers, before you commit to anything.