DSN Payroll Outsourcing in France

If your French subsidiary missed a DSN deadline last quarter, you already know the answer to the question this page exists to answer: the Déclaration Sociale Nominative is not a payroll detail, it is the central nervous system of French employer compliance. Miss it, file it wrong, or trust it to a provider who treats it as routine, and the consequences arrive faster than you expect.

This page explains what the DSN is, what it costs to get wrong in 2026 (including the new automatic substitution mechanism that activated in March), and what a competent payroll outsourcing partner actually delivers when you hand the DSN to them.

What the DSN is, in one paragraph ?

The Déclaration Sociale Nominative (DSN) is the single monthly digital filing that French employers must send to URSSAF, France Travail, the CPAM, supplementary pension funds (Agirc-Arrco), provident schemes, and the tax authority, all in one transmission. It carries every employee's identity, contract data, gross pay, social contributions, working time, leave events, and personal income tax withholding. It was made mandatory for all private sector employers under the general scheme on 1 January 2017, and replaces more than 80 separate declarations that used to circulate between employer payroll teams and various French agencies. Source of authority: URSSAF DSN portal and entreprendre.service-public.gouv.fr.

A DSN is generated by your payroll software (Silae, Cegid, ADP, Sage, PayFit, and a handful of others certified to the NEODeS 2025.1 standard that has been in force since January 2025), then transmitted via net-entreprises.fr or via API directly from the payroll engine.

AUDIT

ACCOUNTING

TAXATION

What the DSN actually contains ?

A monthly DSN bundle carries far more than salary data. It includes:

Identity and employment contract for every active employee (NIR, contract type, working hours, position)

Gross salary, all components of remuneration, benefits in kind, bonuses, expense reimbursements

Computed social contributions for URSSAF, Agirc-Arrco, unemployment, work accident insurance, CSG/CRDS, mutuelle, prévoyance

Personal income tax withheld at source (PAS) at the rate transmitted by the tax authority

Life-cycle events: hires, terminations, sick leave, maternity, paternity, work accidents, contract amendments

Working time accounting per employee

In total, the NEODeS 2025.1 specification carries more than 500 distinct data fields. This is why DSN is not a clerical task. It is a structured data engineering exercise with a legal liability tail.

There are two types of DSN:

Monthly DSN (DSN mensuelle) carrying remuneration, contributions, and PAS for the calendar month

Event DSN (DSN événementielle) carrying specific employee events that must be reported within 5 working days of occurrence (typically sick leave or end of contract)

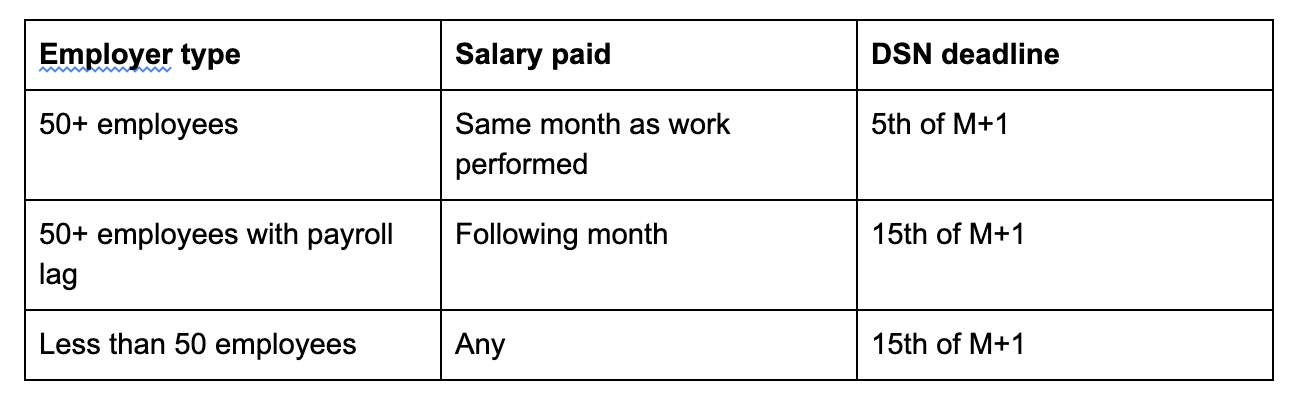

2026 deadlines: the rule that everyone gets wrong

2 filing deadlines exist, and which one applies depends on headcount and salary timing.

Concrete example, straight from URSSAF guidance: a company of 52 employees that pays April salaries on 28 April must transmit the April DSN by 5 May. The same company, if it pays April salaries on 5 May, must transmit by 15 May.

If the deadline falls on a weekend or public holiday, it shifts to the next working day. You do not get to choose your date. The 5th-versus-15th decision flows from your effective payroll schedule, and changing it requires prior notification to URSSAF (a Cour de Cassation ruling that catches many international groups off-guard).

2026 penalty grid: what missing a DSN actually costs

The penalty regime is set by articles R243-12 and R243-13 of the Code de la Sécurité Sociale, indexed on the monthly social security ceiling (PMSS, set at 4 005 EUR for 2026).

Headline figures for 2026:

Failure to transmit a DSN at all: 20.02 EUR per employee (flat-rate simplified penalty)

Late transmission: 60 EUR per employee per month, or fraction of a month, of delay. Capped at 6 008 EUR per company per month if delay is 5 days or less, applicable once per calendar year

Omission of an employee from the DSN: 1.5% of PMSS per missing employee per month

Inaccurate remuneration declaration: 40.05 EUR per error

Late payment of social contributions: 5% surcharge plus 0.20% interest per month

A 30-day right-to-error mechanism (droit à l'erreur) can cancel certain penalties for a first offense in good faith, on condition the company has had no infraction in the previous 24 months and corrects the situation within 30 days of the notification.

For a 25-employee subsidiary that misses a single DSN by two weeks, the calculation is straightforward and unforgiving: 25 × 60 EUR = 1 500 EUR for the month, plus 5% on contributions, plus interest. Repeat that across two filings and you are above 4 000 EUR for an entirely preventable error.

The 2026 shift you cannot afford to miss: DSN de substitution

This is the part most foreign-language sources have not yet caught up on, and the part that should change how you think about DSN governance starting now.

Since March 2026, URSSAF has activated a new mechanism called DSN de substitution. The principle: if URSSAF detects anomalies in your monthly DSN filings, raises them in the CRM (Compte Rendu Métier) monthly feedback files, and the anomalies are not corrected within the regularisation window (typically a March-to-May window each year following the annual reminder CRM), URSSAF will issue a substitute DSN of its own, overwriting your declaration and locking in the corrected data without your consent.

The first wave focuses on anomalies that affect basic and supplementary pension rights. Future waves will extend to other domains.

What this means in practice:

The grace period that informally existed when CRM warnings were ignored is gone

URSSAF takes editorial control of your social declarations once you cross the threshold

The corrections come with retroactive contribution adjustments, late-payment surcharges, and a permanent compliance record

It is the textbook signature of a payroll function that has lost control

Sources: URSSAF official communication and the Service-Public detailed page.

If your French DSN flow has had recurring anomalies for the past two years, you are in the active firing line. This is the moment to either rebuild the process internally with a senior payroll lead or hand the file to an outsourcing partner who will close the gap before June 2026 lands.

Why outsourcing the DSN flow is the right move for most foreign groups ?

The internal-versus-outsourced debate has shifted. With NEODeS 2025.1 active, automatic CRM controls reinforced, and substitution DSNs now possible, internalising DSN inside a non-French parent is a structurally fragile choice. Three reasons:

Regulatory drift outpaces internal training. French payroll rules update at least twice a year, and the DSN technical specification rewrites roughly annually. Maintaining a single internal payroll lead in Paris who tracks all of it is feasible. Backstopping that lead during sick leave, holidays, or turnover, while keeping the parent in the loop, is where most internal setups fail.

Software certification matters. Only payroll engines certified for the current DSN norm can transmit cleanly. Switching cost is real. An outsourcing partner with multi-client investment in a certified engine spreads the cost.

The cost of one URSSAF audit triggered by DSN anomalies typically exceeds three years of outsourcing fees. This is not theoretical. Vachon clients who came to us after a DSN-driven audit faced retroactive contribution recoveries, surcharge interest, and consultant fees that ran into six figures. Outsourcing is a risk-transfer instrument before it is a productivity tool.

For a broader view of when payroll outsourcing pays off, see our payroll outsourcing in France service page.

What a competent DSN outsourcing partner actually delivers

This is where most service brochures lose specificity. Here is the operational checklist that separates a real DSN partner from a payslip mill.

Pre-filing controls

Reconciliation of payroll data with HR system (SIRH) before each closing

Application of the right collective bargaining agreement, including its salary minima, allowances, and CBA-specific rubrics

PASS ceiling computation and tranche allocation

Verification that personal income tax rates received from DGFiP have been correctly mapped per employee

Cross-check of working time, leave, overtime against contract terms

Monthly filing operations

DSN file generation in NEODeS 2025.1 from the certified payroll engine

Transmission via net-entreprises.fr or API

Reception and review of monthly CRM (Compte Rendu Métier) returned by URSSAF

Immediate analysis of any anomalies flagged in the CRM, with a short-cycle correction plan

Annule-et-remplace procedure if an error is detected before the deadline

Block-de-régularisation correction on the following month's DSN if detected after deadline

Annual cycle and audit posture

Review of the annual reminder CRM (CRM de rappel annuel) issued in March

Active correction of any remaining anomalies during the March-to-May window to prevent a DSN de substitution

Preparation of supporting evidence files for any URSSAF audit

Liaison with the parent group on reconciliation between French statutory accounts and group reporting

Specific events handled

Event DSN within 5 working days for sick leave, terminations, contract changes

Final settlement calculations for departing employees (solde de tout compte, severance indemnities, RTT and paid leave balances)

Onboarding declarations (DPAE) and exit declarations

Bridging with payroll audit services when an inspection is announced

A provider that cannot articulate this list with the same level of precision is not running a DSN service. They are running a payslip-printing operation with DSN as a side effect. The difference matters in the audit room.

Decision framework: what to ask a DSN provider before signing

Five questions that filter the market quickly.

1. Which DSN-certified payroll engine do you operate? The right answers in 2026 are Silae, Cegid, ADP, Sage, or a similarly certified product. If they cannot name it, walk away.

2. How are CRM anomalies escalated to my finance team? Look for a defined SLA, ideally 48 hours from CRM receipt. A monthly newsletter is not an escalation procedure.

3. What is your written policy on the DSN de substitution risk window? Any provider serious about 2026 should have a documented protocol for the March-to-May regularisation window.

4. Who is the named senior payroll professional on my account? The DSN is not a junior task. The lead on your file should hold a payroll specialist qualification or equivalent (Titre Professionnel Gestionnaire de Paie, or supervised by an Expert-Comptable inscrit à l'Ordre).

5. How do you reconcile French data with parent reporting under US GAAP, UK GAAP, or IFRS? This is where most pure-play payroll providers stop and where a CPA firm starts. Our French and US GAAP reconciliation methodology is the structural answer for groups that need both.

Specific case: foreign employer with no French entity

If your company has no establishment in France, the standard URSSAF DSN flow does not apply directly. You file either through the TFE (Titre Firmes Étrangères) simplified portal managed by URSSAF Alsace, or via a fragmented DSN if you use a payroll provider. We have a dedicated page on foreign employer payroll in France that walks through the registration process, the choice between TFE and DSN, and the specific exemptions you can claim under article L.6131-1 of the Labour Code.

Why foreign groups bring DSN outsourcing to Vachon

Three reasons that we hear back from CFOs after onboarding.

Senior CPA oversight on every file. Vachon is a chartered accountancy firm (Expert-Comptable inscrit à l'Ordre, Commissaires aux Comptes), founded in 1997, with a team of around 40. DSN is processed under the supervision of a senior practitioner, not a back-office function. When URSSAF calls, the answer comes from a partner.

Bilingual operations across French and English. The monthly summary your parent group receives is built for finance leadership in London, New York, Munich, or Tokyo. We translate French statutory reality into the language and accounting framework your group uses.

Integration with the rest of the French compliance stack. DSN sits inside a wider compliance perimeter that includes corporate tax, VAT, statutory accounts, transfer pricing documentation, and audit support. Running them under one firm closes the seams that often cost foreign groups the most. See our payroll and tax management services page for the integrated view.

We do not run a global EOR. We do not operate a HR-tech SaaS. We are a Paris-based CPA firm that files clean DSNs for foreign-owned French entities, month after month, with a bias toward audit-ready documentation.

Frequently asked questions

What is the DSN in French payroll?

The Déclaration Sociale Nominative is the single monthly digital filing that consolidates payroll, social contribution, and personal income tax withholding data for every employee, transmitted via net-entreprises.fr to URSSAF and other French social agencies. It has been mandatory for all private-sector employers under the general scheme since 1 January 2017.

When is the DSN due?

By the 5th of the following month for employers with 50 or more employees paying salaries within the same month, or by the 15th of the following month for employers under 50 employees and for larger employers operating with a payroll lag.

How much does a late or missing DSN cost in 2026?

Failure to transmit triggers a 20.02 EUR per employee penalty. Late transmission costs 60 EUR per employee per month of delay, capped at 6 008 EUR per company per month for delays of 5 days or less. Errors and omissions add layered penalties under articles R243-12 and R243-13 of the Code de la Sécurité Sociale.

What is the DSN de substitution introduced in 2026?

A new mechanism, active since March 2026, by which URSSAF can issue a corrective DSN on the employer's behalf when anomalies flagged in monthly CRMs are not resolved within the annual regularisation window. The first wave targets anomalies affecting employees' pension rights.

Can a foreign company without a French entity file a DSN?

Yes, through the simplified TFE (Titre Firmes Étrangères) portal managed by URSSAF Alsace, or through a standard DSN flow with a French payroll provider. The choice depends on the volume and complexity of the payroll.

How long does it take to outsource DSN filing to a new provider?

A clean transition from in-house to outsourced DSN typically takes 4 to 8 weeks: data migration, payroll engine configuration, CBA mapping, validation parallel run, and live cutover. Mid-year transitions are possible but should avoid the March-to-May regularisation window.

What happens to past DSN errors when we change provider?

A serious incoming provider audits the prior 24 months of DSN filings, identifies open CRM anomalies, and corrects them through the block-de-régularisation mechanism in the next monthly DSN. Pre-existing DSN de substitution risk should be flagged and remediated immediately.

Is DSN outsourcing the same as Employer of Record?

No. DSN outsourcing applies when you are the legal employer (through your French entity or your registered foreign-employer status) and you delegate the declaration and contribution flow to a third party. An Employer of Record becomes the legal employer in your place. The two answer different questions.

Hand the DSN to a partner who treats it as a controlled process

If your DSN flow has had recent CRM anomalies, if your French payroll lead is overstretched, or if you are reading this because a URSSAF letter just landed in your inbox, the conversation is worth having now rather than later. We can run a 2-hour DSN diagnostic on your last 12 filings, score the residual risk, and give you a fixed-fee remediation plan before the June 2026 substitution window applies.